Starting a home renovation is an exciting prospect, but figuring out how to pay for it can feel like a huge hurdle. That's where a home renovation loan comes in. It’s a specific type of financing designed to bring your vision to life without you having to drain your savings account. Think of it as a financial partner for your remodel, one that helps you invest directly in your property's value and your family's comfort.

Funding Your Dream Project with Home Renovation Loans

Embarking on a remodel is a major investment, not just in your house, but in your quality of life. Whether you're in Monterey, CA, dreaming of a new coastal-style kitchen or you're over in Maricopa County, AZ, planning a backyard oasis, the right financing makes all the difference. Home renovation loans are what bridge the gap between your current budget and your dream home, giving you the capital you need to get the job done right.

The desire for home upgrades is stronger than ever. The global home renovation market is on track to grow from about $2.05 trillion in 2025 to a massive $2.66 trillion by 2032. North America is leading the charge, making up roughly 33.34% of that market. This just goes to show how many homeowners rely on smart financing to fund their ambitious projects. You can read more on these home renovation market trends to get the full picture.

Why Financing Is a Smart Choice

Opting for a loan instead of paying cash out-of-pocket can be a strategic move. It lets you keep your savings intact for emergencies, tackle a more substantial and impactful renovation, and potentially boost your home's value in a big way.

A well-planned remodel doesn't just make your day-to-day life better; it can also deliver a solid financial return. For instance, updating a kitchen with Quartz countertops or adding an energy-efficient bathroom can make your property much more appealing and increase its market price. Before you start, it's smart to understand the financial side of things, which is why we always recommend exploring your home renovation's return on investment.

A Quick Look at the Main Loan Categories

Finding your way through the world of renovation loans starts with understanding the two main types. Each one serves a different purpose and fits a different financial situation. Here’s a quick overview of the most common options you’ll encounter.

Quick Comparison of Popular Home Renovation Loan Types

| Loan Type | Typical Use Case | Based On | Pros & Cons |

|---|---|---|---|

| Secured Loans | Large-scale remodels, additions, or projects where lower interest rates are a priority. | Your home's equity (the value of your home minus what you owe). | Pros: Lower interest rates, higher borrowing limits. Cons: Puts your home up as collateral, longer application process. |

| Unsecured Loans | Smaller projects, quick repairs, or when you don't have enough home equity. | Your credit score and income. | Pros: Faster funding, no risk to your home. Cons: Higher interest rates, lower borrowing limits. |

These two categories—secured and unsecured—are the foundation of renovation financing.

A secured loan is tied to an asset you own, usually your home. It’s like unlocking your property’s hidden value (its equity) and using it as collateral. Because the lender has that security, these loans typically come with lower interest rates.

On the other hand, an unsecured loan is based purely on your financial reputation—your credit score and income. It doesn't require any collateral, which often makes it a faster option that doesn't put your home on the line, though you'll usually see higher interest rates.

This guide will walk you through these options in more detail, helping you make a confident decision for your project, whether you're in Santa Cruz, San Benito, or anywhere else you call home.

Choosing Your Path: Secured vs. Unsecured Loans

When you start looking at home renovation loans, you’ll quickly find yourself at a fork in the road with two main paths: secured and unsecured loans. Each one is built for different needs, and picking the right one really boils down to your financial situation, how big your project is, and what level of risk you’re comfortable with. Getting this fundamental difference down is the first real step toward borrowing with confidence.

A secured loan is pretty straightforward: it’s financing that uses an asset as collateral. In this case, that asset is your home. Think of it like using your house keys to unlock a vault of funds tied directly to your property’s value. Because you’re putting up that guarantee, lenders see you as a lower-risk borrower, which almost always means you get better terms.

Unlocking Value with Secured Loans

The most common secured loans you'll see for renovations are Home Equity Loans and Home Equity Lines of Credit (HELOCs). For homeowners in high-equity spots like Santa Cruz and Monterey Counties, where property values have shot up, these loans are an incredibly powerful tool. You're basically tapping into the value you've already built up in your home to make it even better.

The main perks of going the secured route include:

- Lower Interest Rates: Because your home guarantees the loan, lenders are willing to offer much more competitive rates.

- Higher Borrowing Limits: You can often borrow a much larger sum, which makes these loans perfect for massive projects like a full kitchen gut, a primary suite addition, or major structural work.

- Potential Tax Deductions: The interest you pay on home equity financing might be tax-deductible if you use the money to "buy, build, or substantially improve" the home that secures the loan [IRS, 2024].

The big thing to remember, though, is that your home is on the line. If you were to default on the loan, your property could be at risk. That's why it's absolutely crucial to make sure the monthly payments fit comfortably in your budget before you sign anything.

The Flexibility of Unsecured Loans

On the other hand, an unsecured loan—which is usually a personal loan—is more like a "handshake" deal based on your financial reputation. Lenders look at your credit history, your income, and your debt-to-income ratio to decide if you qualify and what your interest rate will be. The major advantage here is that no collateral is required.

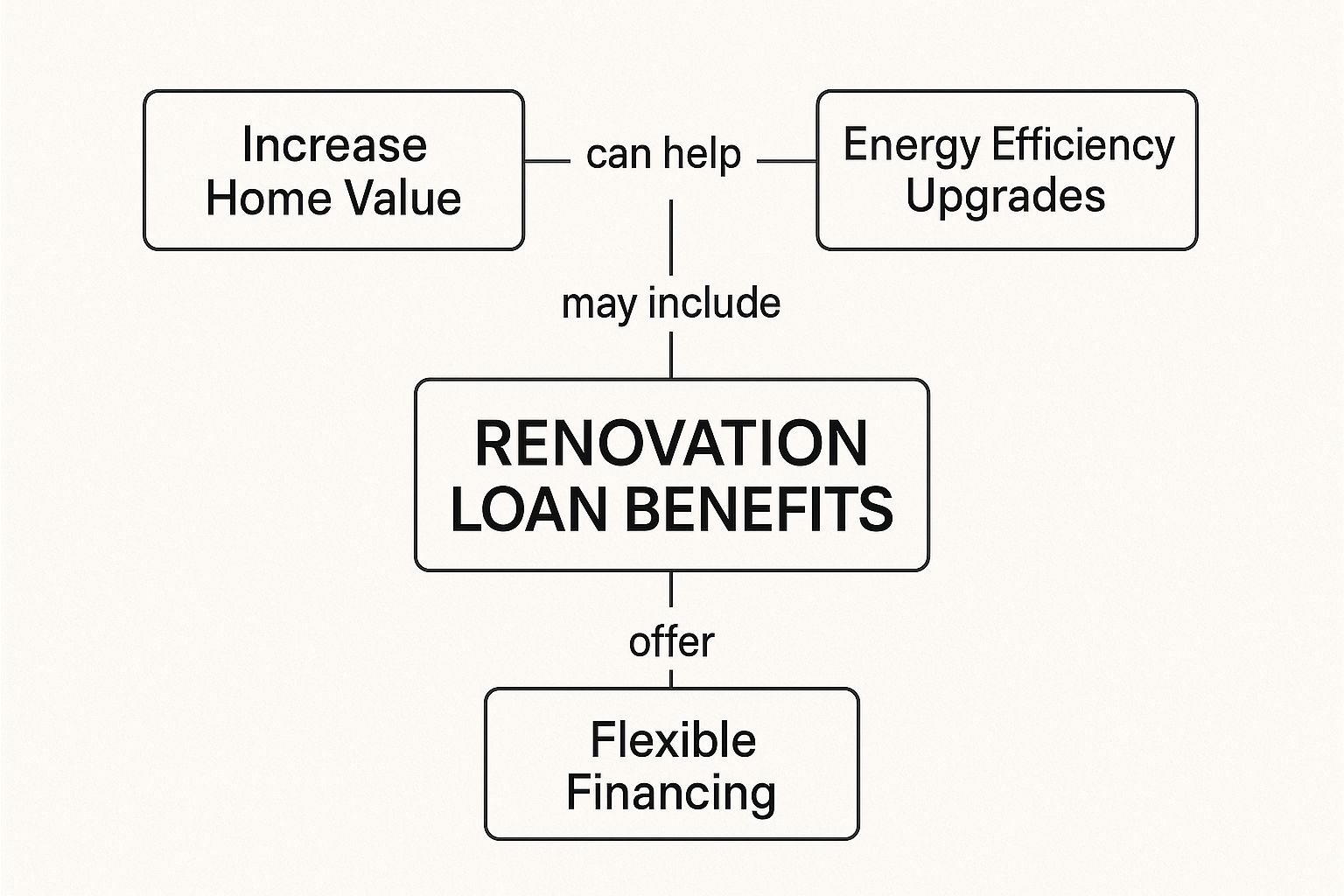

This infographic gives a great visual of how different loans can help you hit your renovation targets.

As the image shows, whether you’re aiming to boost your property's value, make it more energy-efficient, or just need flexible cash for upgrades, there’s a loan out there designed to help you get it done.

Unsecured loans are often the go-to for homeowners who might not have a ton of equity built up yet, or for people who simply value speed and simplicity. The application process is typically much faster, and you can often get the funds in just a few business days. The trade-off for that convenience and lower personal risk is usually a higher interest rate compared to secured loans. For a deeper look, understanding the differences between personal loans and home equity loans can really help you weigh which option is truly best for your project.

A Practical Guide to Your Financing Options

Knowing the difference between secured and unsecured financing is a great start, but the real magic happens when you can pinpoint the exact loan that fits your project like a glove. Choosing the right home renovation loan is one of the most critical decisions you'll make, ensuring your remodel is as stress-free as it is successful. Your financing should be a perfect match for your project's scope, timeline, and budget.

It’s no secret that home improvement is booming. In fact, spending in the US is projected to hit an incredible $509 billion by 2025. This explosion is largely driven by savvy homeowners using their property's value to fund their dream projects. You can discover more insights about the home improvement economic forecast to see just how central financing has become to this trend.

The Best Loan for a Fixed-Budget Project

When you're tackling a big, one-time project with a clear, fixed price tag, the Home Equity Loan is often your best bet. Think of it as getting a single, lump-sum check for your entire renovation. This is perfect for projects like a complete kitchen gut-and-remodel or a new room addition where you have a firm quote from a contractor like Aldridge Construction.

Here’s why it works so well:

- Predictable Payments: You lock in a fixed interest rate, so your monthly payment never changes. This makes budgeting a breeze.

- A Clear Endpoint: You borrow a set amount and pay it back over a defined period. It’s a straightforward path with a clear finish line.

- Ideal for Major Upgrades: It gives you the substantial cash you need upfront for those transformative projects that dramatically increase your home’s value.

This option is a fantastic fit when you know the total cost ahead of time, which helps keep your spending on track.

When Your Project Needs Flexibility

But what if your renovation is more of an evolving process? Maybe it’s happening in phases, or you want the freedom to tackle issues as they arise. This is where a Home Equity Line of Credit (HELOC) truly shines. A HELOC works a lot like a credit card that’s secured by your home. You’re approved for a maximum credit limit, but you only draw—and pay interest on—the funds you actually use, when you use them.

A HELOC is perfectly suited for long-term projects with evolving costs, such as a backyard landscape transformation in Maricopa County or a series of cosmetic updates throughout a home in Monterey. It gives you the financial agility to handle unexpected expenses without needing to reapply for a new loan.

Before diving headfirst into loan applications, it’s smart to get a handle on your overall financial picture. A solid guide to financial planning can give you the foundation you need to make the best choice for your renovation. This groundwork ensures that whichever loan you pick, it fits comfortably within your long-term goals.

Government-Backed and Specialized Loans

Beyond the usual equity-based options, there are several specialized loans backed by the government. These can be incredible tools, especially if you’re buying an older home that needs work or focusing on specific types of improvements.

- FHA 203(k) Loan: This is the ultimate "fixer-upper" loan. It lets you roll the cost of buying a home and renovating it all into a single mortgage. It’s a game-changer for buyers who see amazing potential in a property that needs a lot of love.

- Fannie Mae HomeStyle® Loan: This is similar to the 203(k) loan but offers more flexibility. It’s great for financing cosmetic upgrades and even luxury improvements—like a pool or high-end finishes—that an FHA loan might not cover.

- VA Renovation Loan: For our eligible veterans and service members, this loan is a powerful tool. It provides a path to finance home improvements with the potential for 100% financing, making renovations incredibly accessible.

These programs show just how many different paths there are to funding your project.

Local Considerations for Your Loan Amount

As you figure out how much to borrow, don't forget to factor in local requirements. For homeowners in Monterey or San Benito County, California’s Title 24 energy standards can directly impact your project's bottom line. Upgrades like installing energy-efficient Milgard windows or adding better insulation might be required, and those costs need to be in your budget.

Likewise, pulling the right permits is a non-negotiable step for any significant remodel. The cost and time involved in this process absolutely must be part of your loan calculation. Taking the time to understand local construction permit requirements is key to building an accurate budget and keeping your project on schedule. Here at Aldridge Construction, we help you account for these local factors from day one.

How to Navigate the Loan Application Process

Applying for a home renovation loan can feel a bit daunting, but if you break it down into a clear roadmap, the entire journey becomes predictable and much less stressful. Think of it like building your project's financial foundation, one solid step at a time. By approaching it methodically, you put yourself in the driver's seat to secure the best possible terms for your project in Monterey, Santa Cruz, or Maricopa County.

The real work actually begins long before you even fill out an application. It starts with getting your financial house in order so you look like a reliable borrower. After that, you'll move into the active steps of gathering quotes and seeing what different lenders have to offer.

Step 1: Assess Your Financial Health

Before you let any lender peek at your finances, you need to understand exactly where you stand. This boils down to two key numbers: your credit score and your debt-to-income (DTI) ratio. Lenders lean heavily on these metrics to gauge how well you can handle new debt.

Your credit score is basically a snapshot of your borrowing history. A higher score often unlocks lower interest rates, which can save you a small fortune over the life of the loan. Most lenders consider a score of 740 or above to be excellent, opening the door to the most attractive home renovation loans.

You're entitled to a free credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) every year. It’s smart to pull them, check for any errors that could be dragging your score down, and dispute them right away.

Step 2: Organize Your Paperwork

Once you have a handle on your credit situation, it's time to gather all the necessary documents. Lenders need a detailed look at your financial history to verify your income and assets. Being organized here is a game-changer and can seriously speed up your application.

Start a dedicated folder—digital or physical—and start collecting these essentials:

- Proof of Income: This usually means your last two years of W-2s and your most recent pay stubs covering a 30-day period.

- Tax Returns: Lenders will want to see your federal tax returns for the past two years.

- Bank Statements: Grab the last two to three months of statements for all your checking, savings, and investment accounts.

- Debt Information: Make a clear list of all your current debts, like car loans, student loans, and credit card balances.

Step 3: Secure a Detailed Contractor Quote

This is a huge one. In fact, it's probably the most critical step in the whole process. Lenders need to see a professional, itemized quote that clearly lays out the scope of work, material costs, and labor expenses. A vague estimate just won't fly; they need to feel confident that the loan amount you're asking for matches the project's real cost.

This is where partnering with an experienced general contractor like Aldridge Construction gives you a massive advantage. We build detailed, lender-ready proposals that break down every single aspect of your remodel. This not only satisfies the lender's requirements but also protects you from budget blowouts down the line.

Step 4: Compare Lender Offers and Complete the Process

With your financial documents and contractor quote ready to go, you can officially start shopping for your loan. Don't just jump on the first offer you get. Take the time to compare rates and terms from different places, including local banks, credit unions, and reputable online lenders.

After your home renovation loan gets the green light, the last piece of the puzzle is the loan signing. This is a crucial step that can often be streamlined with professional loan signing services. From there, you'll finish the lender's underwriting process, where they do one final check of all your info before funding the loan. With these steps complete, you’ll be ready to break ground on your dream renovation.

What Lenders Look for When You Apply

When you apply for a home renovation loan, lenders pull back the curtain on your financial life. They need to decide if you’re a reliable borrower, and they don’t just look at one number. Instead, they’re sizing up your entire financial picture using a framework often called the “Five C’s of Credit.”

Knowing what they’re looking for demystifies the whole process. It helps you get your ducks in a row and put together an application that’s built for success. Each “C” gives the lender a different piece of the puzzle, helping them gauge the risk of handing you tens or even hundreds of thousands of dollars for your project.

Character: Your Financial Reputation

First up is Character, which is just a lender’s way of talking about your credit history. They’ll pull your credit report to see how you’ve managed debt in the past. Have you consistently paid your credit cards, car loans, and mortgage on time? A clean track record is what they want to see.

Your credit score is the most direct proof of good character. While it's possible to get a loan with a lower score, 740 or higher is the magic number. Hitting that mark usually unlocks the best interest rates and terms, saving you a boatload of money over the life of the loan.

Capacity: Your Ability to Repay

Next, they look at Capacity—your ability to comfortably handle another monthly payment. Lenders figure this out by calculating your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A low DTI tells them you have enough cash flow to take on the new loan without getting stretched too thin.

Most lenders like to see a DTI ratio below 43%, and that includes the payment for your new renovation loan. It’s a key signal that you have the financial breathing room to manage your obligations.

Capital: Your Skin in the Game

Capital is all about the personal funds you have on hand, like your savings, investments, or a down payment. Having capital shows lenders that you’re financially stable and have some of your own "skin in the game." It proves you aren't relying entirely on borrowed money to fund the project or cover any unexpected bumps in the road.

While some renovation loans come with low or even no down payment options, having savings ready to go is always a huge plus in a lender's eyes. It’s your financial safety net, and it shows you’re a responsible borrower who plans ahead.

Collateral: The Value of Your Home

For secured loans like a HELOC or home equity loan, Collateral is everything. This is the asset you’re pledging to back the loan—in this case, your house. A professional appraiser will determine your home's current market value, which sets the limit on how much equity you can borrow against.

Because the lender can make a claim on your property if you default, their risk is much lower. This is exactly why secured loans almost always come with better interest rates than unsecured personal loans.

Conditions: The Purpose of the Loan

Finally, lenders look at the Conditions of the loan. This includes what you plan to use the money for, the total amount you’re asking for, and even the broader economic climate. For a renovation loan, your purpose is straightforward: you're improving your property. This is where a detailed, professional contractor quote becomes your best friend.

Handing over a clear, itemized bid from a reputable firm gives the lender a massive dose of confidence. It shows them the funds are earmarked for improvements that will likely increase the home’s value, making their investment much more secure. If you’re not sure where to start, our guide on how to find a good contractor is a fantastic resource.

The market outlook for home improvement lending is still strong. With mortgage rates on the higher side, more homeowners are choosing to renovate instead of move, which keeps the demand for these loans steady. You can learn more about the 2025 structured finance outlook to see how lenders are approaching the market.

Partner with Aldridge Construction for a Seamless Renovation

Getting your home renovation loan approved is a huge first step, but let's be honest—it’s only half the battle. The real magic happens when that financing is turned into a beautiful, well-built reality. That’s where Aldridge Construction comes in. We bridge the gap between your financial green light and your finished project with the expertise and integrity you deserve.

Choosing the right contractor is just as critical as picking the right loan. In fact, a lender’s decision often comes down to the quality and detail of your contractor's proposal. We specialize in creating the kind of comprehensive, itemized quotes that bankers love to see—clear, detailed, and outlining every single cost. These lender-ready documents are built to satisfy even the strictest financial requirements, smoothing your path to approval.

Your Local Project Partner in CA & AZ

Our deep roots in Monterey, Santa Cruz, and San Benito Counties in California, as well as Maricopa County, Arizona, give our clients a serious advantage. We have a ground-level understanding of the regional building codes, permit fees, and material costs that absolutely must be factored into your loan from day one. This local knowledge helps you sidestep the costly surprises and frustrating delays that can derail a project.

From navigating California’s Title 24 energy codes to sourcing the right materials for the Arizona heat, our team manages all the complexities. This frees you up to focus on the exciting part: watching your dream home finally take shape.

Ready to see how we work? A successful remodel starts with a solid plan. Explore our approach to custom home renovation to see how we deliver exceptional results time and again.

FAQs: Your Home Renovation Loan Questions Answered

How much can I borrow for a home renovation?

The amount you can borrow depends on the loan type, your finances, and your home's value. For a home equity loan or HELOC, lenders typically allow you to borrow up to 85% of your home's appraised value, minus your outstanding mortgage balance. For unsecured personal loans, borrowing limits are based on your credit score and income, usually ranging from a few thousand dollars up to $100,000.

Can I get a renovation loan with bad credit?

While more challenging, it's not impossible. Government-backed programs like FHA 203(k) loans often have more lenient credit requirements than conventional loans. However, be prepared for a higher interest rate. The best strategy is to work on improving your credit score before applying to secure better terms.

Should I choose a HELOC or a Home Equity Loan?

This depends on your project's structure. A Home Equity Loan is ideal for a single, large project with a fixed budget, like a complete kitchen remodel in your Santa Cruz home, as it provides a lump sum with predictable payments. A HELOC is better for phased projects or when you need flexibility for unexpected costs, acting like a credit line you can draw from as needed.

How long does it take to get a renovation loan?

Timelines vary. Unsecured personal loans are fastest, often funding within a few business days. Secured loans like a HELOC or home equity loan take longer—typically 30 to 45 days from application to funding—because they require a full home appraisal and detailed underwriting.

Do I need a contractor quote before I apply?

Yes, for most renovation-specific loans, a detailed contractor bid is non-negotiable. Lenders require a professional, itemized quote to validate the loan amount and ensure the funds are used for value-adding improvements. Working with experienced home improvement contractors like Aldridge Construction ensures you get a detailed proposal that lenders will accept, setting your project up for a smooth start.

Ready to turn your renovation plans into a reality? A solid plan starts with a professional partner. The team at Aldridge Construction provides the detailed, lender-ready proposals you need to secure financing and expertly manages your project from start to finish. Contact us today for a consultation.