So, you're dreaming of that home addition or backyard ADU in 2025? It's a fantastic idea. And yes, you can afford it—but not with the old financing playbook. With home values on the rise, these projects are smart investments.

The secret is knowing how to fund them in today's market. You need to look at creative financing options like home equity loans and renovation-specific loans, instead of yesterday's go-to cash-out refi.

The 2025 Remodeling Challenge

In high-value areas like Monterey County, CA, and Maricopa County, AZ, homeowners have a lot of potential. Adding a guest house, a modern kitchen, or an Accessory Dwelling Unit (ADU) makes sense. These projects add space and increase your property's value.

But the financial world has changed. For years, the default move for funding a major project was a cash-out refinance. Today, with higher interest rates, that option is less attractive.

Moving Beyond Old Financing Habits

This is where many homeowners get stuck. They see today's rates, think about old methods, and wonder if their dream remodel is possible. The truth is, the old playbook doesn’t work for most people right now.

A recent industry report showed that only 9% of homeowners plan to use a cash-out refinance. That’s a big drop from 24% the year before. This change has created a knowledge gap.

Homeowners need practical, modern financing strategies that make sense today. The good news is that there are powerful alternatives. This guide will help you understand them and answer the big question: how can you afford your home addition in 2025?

At Aldridge Construction, our team believes financial uncertainty shouldn't be a roadblock. We help our clients understand and navigate modern solutions so you can move forward with confidence.

Why This Matters for Your Project

Figuring out your funding strategy is as important as the blueprints. Without a solid financial plan, great designs can end up on the shelf. Aldridge Construction aims to provide real-world solutions to make your project a reality.

Our team doesn't just build—we guide you through the entire journey. We help you make sense of the process, including:

- Exploring Creative Financing: We can connect you with lenders who understand renovation and ADU construction loans.

- Navigating Local Grants: We stay updated on programs in California and Arizona that can lower your project cost.

- Accurate Budgeting: We provide detailed, professional quotes that lenders need to approve your loan.

Before you apply for a loan, the first step is to get organized. A home remodel checklist is a great tool to define your project's scope and priorities.

Using Your Home Equity to Fund Your Project

For most homeowners in Monterey and Santa Cruz Counties, your home is your biggest financial asset. The equity you've built is a powerful tool. It can be the most direct way to fund your home addition or ADU.

Using your home as collateral often lets you secure large loans at better interest rates. The two main options are a Home Equity Loan (HEL) and a Home Equity Line of Credit (HELOC). They sound similar but work differently.

The right choice depends on your project's scope, budget, and payment preferences. Before you can use that value, you need to know what you're working with. A great first step is learning how to determine your current home equity.

Understanding The Home Equity Loan (HEL)

Think of a Home Equity Loan as a second mortgage. You borrow a set amount against your equity and get it all at once. This is a great option when you know the final cost of your project.

Homeowners like a HEL for its stability. It has a fixed interest rate and a predictable repayment schedule. Your monthly payment will never change, which helps with budgeting.

This is the perfect tool for large, well-defined projects. For example, when Aldridge Construction gives you a detailed, fixed-price contract for a home addition or ADU build.

The Flexibility Of a HELOC

A Home Equity Line of Credit (HELOC) is different. It works like a credit card, with your home as security. You are approved for a maximum credit limit and can draw money as you need it.

The key difference is the variable interest rate. This means your payments can change with the market. While this adds uncertainty, it also offers flexibility.

You only pay interest on the amount you’ve used. This is a major advantage for projects with staggered costs. A HELOC is ideal for a kitchen remodel in San Benito County where you might make changes along the way.

Home Equity Loan Vs HELOC At a Glance

So, which one fits your project and financial style? A side-by-side comparison can make the decision clearer. Here's a quick breakdown of the key differences.

| Feature | Home Equity Loan (HEL) | Home Equity Line of Credit (HELOC) |

|---|---|---|

| How You Get Funds | One single lump sum payment upfront. | Draw funds as needed, like a credit card. |

| Interest Rate | Fixed rate that never changes. | Variable rate that can fluctuate. |

| Best For | Projects with a known, fixed cost. | Projects with an evolving or uncertain scope. |

| Payment Structure | Predictable, stable monthly payments. | Payments can change over time. |

Making the right choice is a critical part of your financial planning. To learn more about financing, check out our guide on https://aldridgeconstruction.biz/home-renovation-loans/. The Aldridge Construction team provides clear project proposals that lenders need to help you secure financing.

Diving Into Construction and Renovation Loans

When your plans are big—like a new ADU in Monterey County or a major home addition in Maricopa County, AZ—you need a special loan. A standard mortgage is designed for an existing house, not one from blueprints. This is where construction and renovation loans come in.

These loans follow the building process. They manage the cash flow of a major build, protecting both you and the lender. Money is available when it's needed for materials like lumber, labor, and permits.

How Do These Loans Actually Work?

A construction loan uses a draw schedule. The lender releases funds in stages, or “draws,” as construction milestones are met. For example, the first draw might cover site preparation and the foundation.

Once Aldridge Construction completes that phase and it passes inspection, the bank releases the next payment for framing. This step-by-step approach provides oversight. It shows the lender that work is progressing as planned.

After your project is finished, the loan usually converts into a normal, long-term mortgage. This is often called a construction-to-permanent loan. It bundles two loans into one, saving you time and money.

The Main Types of Renovation Loans

There are several loan products designed for building and major remodels. Each has its own rules and is better for different situations.

- FHA 203(k) Loan: This government-backed loan includes the home purchase and renovation costs in one package. It's great for fixer-uppers because the loan is based on the home's future value.

- Fannie Mae HomeStyle® Loan: This conventional loan is similar to the FHA 203(k). It can be used for a wider range of projects, like adding a swimming pool.

- Construction-to-Permanent Loans: This is the top choice for new construction, like an ADU. It's a single-close loan that covers the build and then becomes a standard mortgage.

Expert Insight: Lenders for construction loans need a detailed plan and a trusted builder. A professional proposal from Aldridge Construction is essential for getting your loan approved.

What Paperwork Will You Need?

Getting a construction loan requires more paperwork than a standard mortgage. The lender is financing a project that doesn't exist yet. They are betting on the future value of your completed addition or ADU.

You will need to provide a complete project plan. This usually includes:

- Detailed Construction Plans: Your architectural drawings and blueprints.

- A Signed Construction Contract: An agreement with your builder that outlines the project scope and timeline.

- An Itemized Budget: A line-by-line breakdown of all expected costs, from concrete to cabinet hardware.

- An Appraisal: A professional assessment of what your property will be worth after the project is finished.

In California and Arizona, lenders will also check that your plans meet local codes, like California's Title 24 energy standards. An experienced local contractor like Aldridge Construction can ensure your application goes smoothly.

Specialized Financing Built for ADUs

An Accessory Dwelling Unit is a unique project that needs a unique loan. A standard home equity loan might work for a kitchen remodel. But building a new living space in your backyard brings up new financial questions.

Because of this, new ADU-specific loan products are now available. They are designed to solve the challenges these projects present. The biggest breakthrough is their ability to consider the ADU’s future rental income when you apply.

For years, this was a major roadblock. Now, some lenders look at the income your new ADU will generate to help you qualify for the loan. This is a game-changer for homeowners.

Tapping Into Local Grants and Incentives

Beyond loans, California homeowners can use local incentives to lower the upfront cost of an ADU. These programs encourage new housing and offer a big opportunity. Taking advantage of these grants can save you thousands of dollars.

One of the best programs is the California ADU Grant Program. It can provide tens of thousands of dollars to cover pre-development costs. These are the expenses you have before construction begins.

The grant typically covers things like:

- Architectural design and blueprints: Professional plans required for permits.

- Engineering reports: Structural, soil, and energy calculations.

- Permit and impact fees: Costs charged by your city or county.

Getting a grant for these early costs makes the project more manageable. It's important to stay on top of these programs, as funding is often limited.

The team at Aldridge Construction stays current on all available ADU grants in Monterey and Santa Cruz Counties. We guide our clients through the application process to maximize funding.

The New Reality of Hybrid Financing

Funding an ADU in 2025 often means getting creative. The most successful creative financing options for ADUs and home additions in 2025 often blend a few strategies. For example, you might use a state grant for design and a construction loan for the build.

These creative solutions are becoming more common. Most lenders still won't count future ADU rental income for a standard mortgage. To fill that gap, homeowners are using a mix of financing options.

Understanding the full financial picture is the first step. That’s why our team offers detailed guidance on the cost to build an ADU. This gives you a realistic budget to take to any lender with confidence.

Alternative Funding Strategies for Smaller Projects

Not every home improvement project is a massive overhaul. What if you’re planning a modest remodel, like a bathroom refresh, but don’t have enough home equity?

There are several good funding strategies for smaller projects. They let you move forward without using your home as collateral. The key is to match the right funding source to your project and budget.

Unsecured Personal Loans

For mid-sized renovations, an unsecured personal loan is a popular choice. It typically covers projects in the $5,000 to $50,000 range. You get this loan based on your creditworthiness, not your home's value.

The biggest advantage is speed. Funding can be approved and in your account within a few days. These loans have fixed interest rates, which means predictable monthly payments.

The trade-off is that interest rates are usually higher than a HELOC or home equity loan. They are a good fit for homeowners who want to keep their home equity untouched.

Using Savings or Credit Cards Strategically

For small projects, like replacing a bathroom vanity, using savings is the most direct method. It’s simple, immediate, and you won’t pay any interest. This is best for minor updates where you can cover the cost without touching your emergency fund.

Credit cards can also be a useful tool, but be careful. A card with a 0% introductory APR offer can be a smart way to finance a small project over several months. This strategy only works if you pay off the balance before the promotional period ends.

Pro Tip: Before starting any project, get a clear idea of the potential costs. Use a tool like our room addition cost calculator to set a realistic budget and choose the right financing.

If your home addition will generate rental income, understanding all funding options is crucial, as explored in this 2025 guide on Short Term Rental Loans. The Aldridge Construction team can help you create a plan that aligns with your budget.

Navigating Your Financing Journey With a Trusted Partner

Choosing how to fund your project is as important as picking out materials like Quartz countertops. After reviewing home equity lines, construction loans, and ADU grants, it's clear there's no single right answer. The best path depends on your finances, project size, and long-term goals.

Answering the big question, "can you afford that remodel?" starts with having a reliable partner. This is where Aldridge Construction is more than just your builder. We help you navigate these complexities by providing accurate cost estimates and professional plans that lenders require.

Reducing Financial Uncertainty

Our knowledge of local permitting in Monterey, Santa Cruz, San Benito, and Maricopa counties helps eliminate costly surprises. We work with you to create a realistic financial plan from day one. This reduces unknowns and lets you focus on the exciting parts of your project.

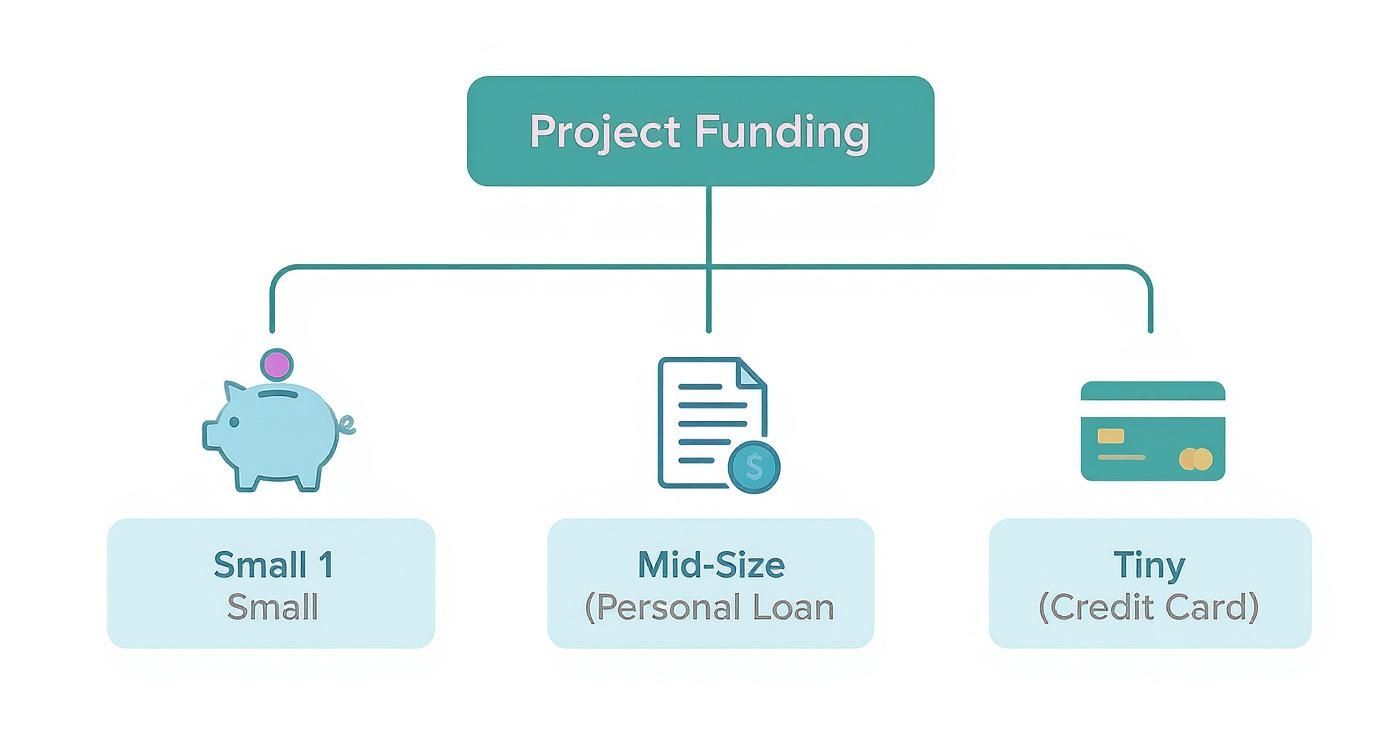

Knowing how to find a good contractor is the first step toward a successful project. A trusted builder provides the clear documentation and oversight that banks need to see. The diagram below shows how to match your project size to a potential funding source.

As you can see, smaller updates might fit savings, while bigger projects require more structured financing.

Building Your Investment With Confidence

The ADU market is booming. Adding an ADU can boost a property’s resale value by nearly 35%, making it a powerful investment. Still, high interest rates and construction costs are real hurdles.

At Aldridge Construction, our team is committed to being a transparent partner. We provide the clear cost breakdowns and professional plans you need to secure financing, turning a complicated process into a manageable one.

Our goal is to ensure your home addition or ADU is not just beautifully built, but also financially sustainable. By working together from the start, we can map out a strategy that aligns your design dreams with your budget.

FAQs: Answering Your Remodel Financing Questions

1. Can I use future ADU rental income to qualify for a loan?

Yes, in some cases. While traditional lenders often don't consider future income, some specialized ADU lenders do. Aldridge Construction works with financial partners in Santa Cruz and Monterey who understand the income potential of ADUs and can help you qualify.

2. How much home equity do I need for a HELOC or Home Equity Loan?

Lenders typically require you to maintain 15-20% equity in your home after the loan. This means you can generally borrow up to 80-85% of your home's appraised value, minus your current mortgage balance. For a home valued at $800,000 with a $400,000 mortgage, you could potentially borrow up to $280,000.

3. Should I get a construction quote or a loan pre-approval first?

It's best to do both at the same time. Getting pre-qualified for a loan gives you a clear budget. Meanwhile, a detailed quote from Aldridge Construction provides the specific numbers your lender needs for final approval, ensuring your plans and budget align perfectly.

4. Are financing rules different in Arizona versus California?

While the core loan types are similar, local factors differ. California has state-level ADU grant programs that Arizona does not. Permit fees, material costs (like for energy-efficient Milgard windows), and timelines can also vary between Maricopa County, AZ, and Monterey County, CA. Our experience in both regions ensures an accurate, location-specific budget.

5. What happens if my project goes over budget with a fixed loan?

This is why a contingency fund is crucial. We recommend setting aside 10-15% of the total project cost in your budget as a safety net for unexpected issues. Aldridge Construction provides detailed quotes to minimize surprises, but if something comes up, we work with you to use your contingency fund or adjust the scope to stay on track.

Ready to stop guessing and start planning? The team at Aldridge Construction is here to provide a clear, detailed estimate for your project, giving you the solid numbers you need to explore your creative financing options. Contact us today to schedule your consultation.